Apparently I’m one of only 5% of Americans who buys health insurance on the individual (non-group) market. I hear that “five percent” figure mostly from politicians trying to downplay the impact of a national Health Insurance Marketplace rollout that has gone hellishly wrong. It’s only affecting 5%. They’re usually accompanied by comments about my legacy health insurance being “cut-rate” or practically worthless, not covering all those “essentials” like pediatric dentistry and maternity.

Trust me, I get it. I’m the tip of the iceberg that the Titanic has already hit. Everyone on a group plan has another year before the disaster strikes your family and you are dropped into this individual marketplace madness.

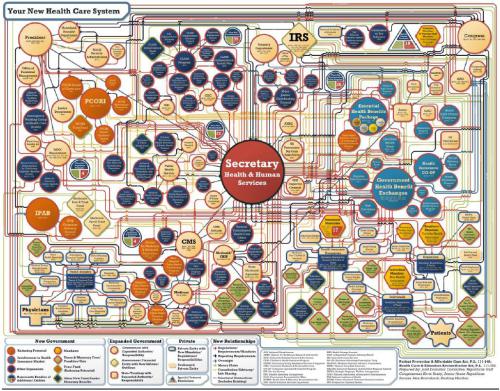

Please don’t think of the Affordable Care Act as a market-based reform. When the federal government mandates certain things be covered (embryo transfer and other reproductive assistance, incidentally, not among them), when they dictate a narrow range of actuarial values such that all plans have almost identical features, when they mandate that insurers offer policies “guaranteed issue” and accept an enormous pool of risky applicants… this is not the way free market works.

You cannot have government tell a market what it has to do and still have it be a market. We’re likely to hear some politician in the near future say something about this rollout to the tune of “well, we tried a market-based solution, and it failed miserably, so the alternative is single-payer…” That may have been the whole purpose from the beginning. Beware. This is socialism.

But I digress. This is the true story of middle class family and their adventure in trying to buy health insurance in the brave new world of Obamacare. Let’s dispatch with the notion their identity needs to be protected (after all, privacy was hardly a concern at healthcare.gov) and just call them the “Gjertsen” family.

John Gjertsen is a financial adviser. He understands the way Obamacare works inside and out, and in spite of its fiscal irresponsibility, he has approached the matter of health insurance personally from a tax planning perspective. Spend 23 minutes with John to learn what taxpayers must understand about buying subsidized health insurance on the Health Insurance Marketplace:

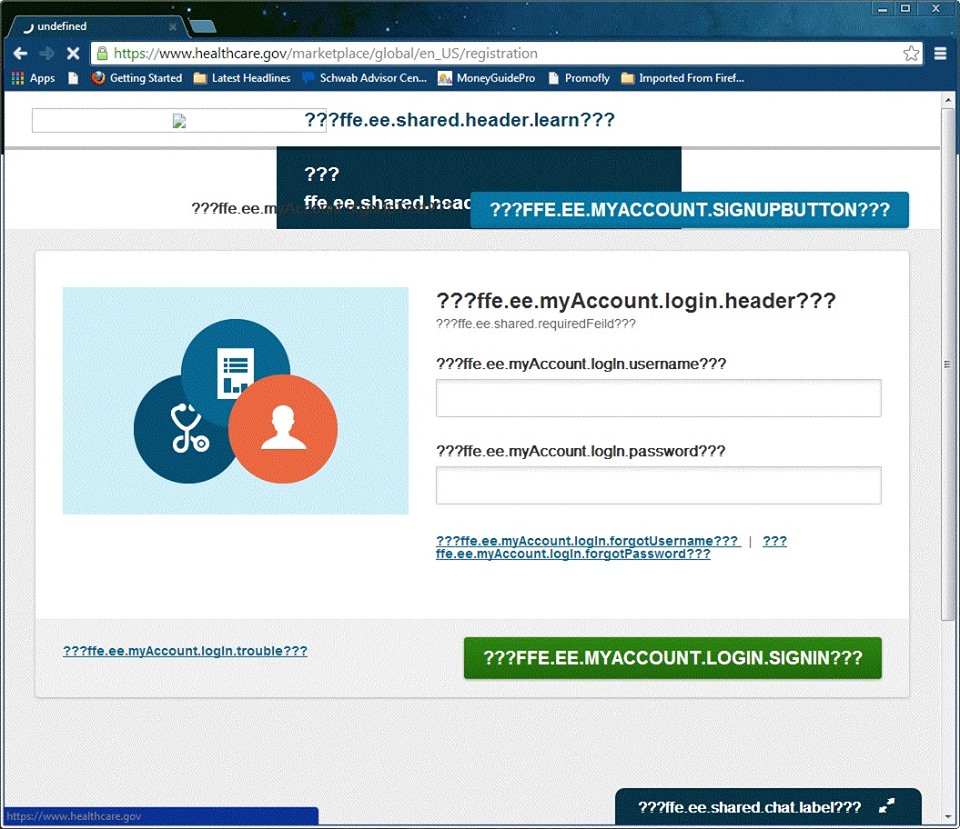

So on October 1, John wakes up and tries to log in and select a plan on healthcare.gov. He’s trying to do this early so that he can assist clients later and let them know what to expect. He actually gets in early in the morning, but the screens start to render text incorrectly, showing coded gibberish.

Later in the day, and later in the week, the site is shut down altogether.

The next week, he’s able to get in, and sometimes, when the site doesn’t completely shut down, he can start the application process. There is no information about actual health insurance, but a lengthy questionnaire ostensibly to determine two things: the size of his family and the income that he expects to report in 2014. But they ask questions about his race, about whether his two sons are related to each other in any way other than siblings, about how much money the toddlers expect to make in 2014, about whether he wants help paying for past medical bills (he thinks “yes” but answers “no”—let’s not make this complicated). He gets to an identity verification step where he actually has to upload a scan of something, the easiest being a voter ID. No problem.

The following week, John tries logging back in to check on his application. Only to discover it is “in progress” and not submitted. To submit it requires going back to square one and answering (or confirming remembered answers to) the same 40 minute application questionnaire. He repeats this process six or seven times, never getting any indication that his application is ever being submitted.

Then he picks up the phone. Turns out they can start over from square one and do the application over the phone. Forty more minutes spent answering the same questions. Little does he know that on the backend, the operator is just using healthcare.gov or something equivalently broken.

He calls back a week later to check the progress of his application. He’s told it has been expedited and he would definitely hear back the following week. When he doesn’t, he calls back. Turns out the application “wasn’t saved in the right area of the system.”

Meaning: it isn’t saved at all. Back to square one. Forty more minutes applying over the phone again. This time, John is told that the result of the application will come not via email, but through the US Postal Service.

October is now over. The official numbers come in and show that that something like 27,000 people have enrolled through the national exchange. Everyone talks about how low that number is, but John scratches his head wonders to himself how it is possible that 27,000 people could have more diligently and resiliently pursued signing up for health insurance than he has.

November brings a new twist: the Chief Executive/Legislator has now decided that John can keep his “cut rate” plan, the one that was so not-worthy-of-being-called-insurance, for one more year. Blue Cross Blue Shield jacks the premium up about 24%, and next to the subsidized exchange plans, which actually cover maternity in a year John’s family might need maternity benefits, it doesn’t sound like a good deal.

John keeps checking his mailbox, expecting to receive something about his application. Nothing. Impatient, John keeps calling the Marketplace to check on the application. In progress. Nothing.

On November 21, John calls the Marketplace again, and learns that his application has been approved! The operator reads from a letter that supposedly was mailed or emailed to John, but that he never received:

Dear John,

You’ve recently submitted an application to the Health Insurance Marketplace. We’ve reviewed your application to see if you can get health coverage through the Marketplace. John, Abigail, Valor, and Grant may all be eligible for Medicaid. You will be receiving a final decision from the North Carolina Division of Medical Assistance. If you do qualify and enroll for Medicaid, you would not qualify for a tax credit and lower copayments, coinsurance, deductibles on Health Insurance Marketplace coverage.

Yes, Medicaid.

How brilliant of them. John is at 239% of FPL, and there is no way his family is going to qualify for Medicaid. But the Marketplace can’t sell him a plan until the North Carolina Division of Medical Assistance officially turns him down. How busy are they? John’s calls to the state do not reach a living person, and the local Craven County Department of Social Services has told him he’s not the only one in this situation, but that he can come into the office and wait in line and go through the motions of applying for Medicaid, offering no assurance this will result in overcoming the latest health insurance application obstacle.

Will the North Carolina Division of Medical Assistance determine in time for John to select a plan and enroll before December 15 23? Seriously, I’m doubtful.

It’s hard writing about John in the third person when I’m personally feeling anxiety and coming to terms with the very real possibility that, in spite of my best efforts, I may not be able to purchase health insurance from this frustrating exchange in time to be covered in January.

Repeal and replace.

Have you considered buying an off-marketplace individual plan? That’s what I did for me and my kiddos and it sounds like it was infinitely easier than the mess you are dealing with! I have a BCBS plan starting 1/1 (with maternity, hooray!) and because I got a Platinum level plan, it has a good network and great benefits, while still costing less than the plan I had the last time I was pregnant. I am certainly not an expert (unless you count switching plans 6 times in 5 years an expert) but after getting denied for my “plan A” group plan and finding myself pregnant without insurance, once my agent figured out from the insurance companies what was going on, I’m happy with my “plan B.” Just thought I would mention it just in case you hadn’t already considered it. (My only frustration has been the mandatory “qualified” pediatric dental, which we decided to ignore until someone could define “qualified” a bit better, and went ahead and purchased a plan for the three of us that cost less than the qualified plan for just my two kiddos.) Good luck!

I’m confused; a Platinum plan *is* a marketplace plan. I think you mean, have I considered just buying it direct from BCBS and not worrying about the subsidies. I have. But that’s crazy expensive ($1328/mo. for Platinum, $770/mo. for the cheapest Bronze, compared to $330/mo. I pay now) Plus I’ve gamed my income through tax deferrals to be at 239% of FPL where I should qualify for not just premium subsidies but cost sharing subsidies, which bring down the deductibles and max out of pocket for Silver plans.

Elections definitely have consequences.

especially primary elections.

I’m so terribly sorry to hear all you’re having to go through on this, on top of all the other recent losses and difficulties.

Is any of this impacted by N. Carolina’s refusal to expand Medicaid? Here in Texas, that’s certainly impacting my sister-in-law and her husband and 3 children. They both work full time with overtime whenever they can get it but still only earn about 125% of the poverty level. She was just told by a benefit coordinator where she works that they won’t qualify for EITHER Medicaid or subsidies on the ACA premiums/deductibles!!

Without subsidies they simply can’t afford any plan and will continue to go forward without insurance at all, she guesses. Thank goodness the family has been very healthy so the risk is relatively low. Still, there’s the occasional problem. Her oldest had a nasty abscess in his ear last August which needed anti-biotics. The trip to the Emergency Room to get a prescription cost $981 which they are still paying off.

Is there any chance your employer will offer health care? Our UHC work plan has steadily increased in cost over the years but is still much less expensive than the individual policy alternatives I saw for our family on ehealthinsurance.com

It’s a mess and I hope your family is able to navigate through it safely.

No, none our difficulties have anything to do with NC not expanding Medicaid; we shouldn’t be qualifying for Medicaid expanded or not.

As far as your sister-in-law, please direct her to the video in this post. At 125% of FPL, if she is able to buy insurance on the new exchanges, their family would get the highest premium credits and cost sharing subsidies. I have a feeling the benefits coordinator gave bad advice.